Ideas

Democrats Need a Critical Minerals Policy Beyond Anti-Trumpism

Party orthodoxy is no longer serving the energy transition, the Breakthrough Institute’s Seaver Wang and Peter Cook write.

Sign In or Create an Account.

By continuing, you agree to the Terms of Service and acknowledge our Privacy Policy

But what happens if the AI boom buffers and data center investment collapses? It is not idle speculation to say that the AI boom rests on unstable financial foundations. Worse, however, is the fact that as of this year, the tech sector’s breakneck investment into data centers is the only tailwind to U.S. economic growth. If there is a market correction, there is no other growth sector that could pick up the slack.

Not only would a sudden reversal in investor sentiment make stranded assets of the data centers themselves, which will lose value as their lease revenue disappears, it also threatens to strand all the energy projects and efficiency innovations that data center demand might have called forth.

If the AI boom does not deliver, we need a backup plan for energy policy.

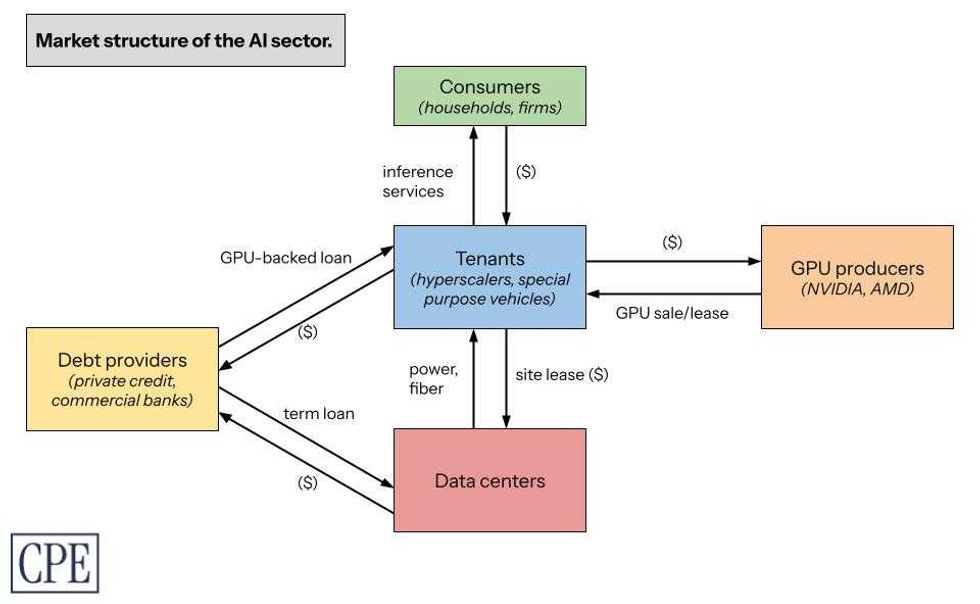

An analysis of the capital structure of the AI boom suggests that policymakers should be more concerned about the financial fundamentals of data centers and their tenants — the tech companies that are buoying the economy. My recent report for the Center for Public Enterprise, Bubble or Nothing, maps out how the various market actors in the AI sector interact, connecting the market structure of the AI inference sector to the economics of Nvidia’s graphics processing units, the chips known as GPUs that power AI software, to the data center real estate debt market. Spelling out the core financial relationships illuminates where the vulnerabilities lie.

Courtesy of Advait Arun

Courtesy of Advait Arun

First and foremost: The business model remains unprofitable. The leading AI companies ― mostly the leading tech companies, as well as some AI-specific firms such as OpenAI and Anthropic ― are all competing with each other to dominate the market for AI inference services such as large language models. None of them is returning a profit on its investments. Back-of-the-envelope math suggests that Meta, Google, Microsoft, and Amazon invested over $560 billion into AI technology and data centers through 2024 and 2025, and have reported revenues of just $35 billion.

To be sure, many new technology companies remain unprofitable for years ― including now-ubiquitous firms like Uber and Amazon. Profits are not the AI sector’s immediate goal; the sector’s high valuations reflect investors’ assumptions about future earnings potential. But while the losses pile up, the market leaders are all vying to maximize the market share of their virtually identical services ― a prisoner’s dilemma of sorts that forces down prices even as the cost of providing inference services continues to rise. Rising costs, suppressed revenues, and fuzzy measurements of real user demand are, when combined, a toxic cocktail and a reflection of the sector’s inherent uncertainty.

Second: AI companies have a capital investment problem. These are not pure software companies; to provide their inference services, AI companies must all invest in or find ways to access GPUs. In mature industries, capital assets have predictable valuations that their owners can borrow against and use as collateral to invest further in their businesses. Not here: The market value of a GPU is incredibly uncertain and, at least currently, remains suppressed due to the sector’s competitive market structure, the physical deterioration of GPUs at high utilization rates, the unclear trajectory of demand, and the value destruction that comes from Nvidia’s now-yearly release of new high-end GPU models.

The tech industry’s rush to invest in new GPUs means existing GPUs lose market value much faster. Some companies, particularly the vulnerable and debt-saddled “neocloud” companies that buy GPUs to rent their compute capacity to retail and hyperscaler consumers, are taking out tens of billions of dollars of loans to buy new GPUs backed by the value of their older GPU stock; the danger of this strategy is obvious. Others including OpenAI and xAI, having realized that GPUs are not safe to hold on one’s balance sheet, are instead renting them from Oracle and Nvidia, respectively.

To paper over the valuation uncertainty of the GPUs they do own, all the hyperscalers have changed their accounting standards for GPU valuations over the past few years to minimize their annual reported depreciation expenses. Some financial analysts don’t buy it: Last year, Barclays analysts judged GPU depreciation as risky enough to merit marking down the earnings estimates of Google (in this case its parent company, Alphabet), Microsoft, and Meta as much as 10%, arguing that consensus modeling was severely underestimating the earnings write-offs required.

Under these market dynamics, the booming demand for high-end chips looks less like a reflection of healthy growth for the tech sector and more like a scramble for high-value collateral to maintain market position among a set of firms with limited product differentiation. If high demand projections for AI technologies come true, collateral ostensibly depreciates at a manageable pace as older GPUs retain their marketable value over their useful life — but otherwise, this combination of structurally compressed profits and rapidly depreciating collateral is evidence of a snake eating its own tail.

All of these hyperscalers are tenants within data centers. Their lack of cash flow or good collateral should have their landlords worried about “tenant churn,” given the risk that many data center tenants will have to undertake multiple cycles of expensive capital expenditure on GPUs and network infrastructure within a single lease term. Data center developers take out construction (or “mini-perm”) loans of four to six years and refinance them into longer-term permanent loans, which can then be packaged into asset-backed and commercial mortgage-backed securities to sell to a wider pool of institutional investors and banks. The threat of broken leases and tenant vacancies threatens the long-term solvency of the leading data center developers ― companies like Equinix and Digital Realty ― as well as the livelihoods of the construction contractors and electricians they hire to build their facilities and manage their energy resources.

Much ink has already been spilled on how the hyperscalers are “roundabouting” each other, or engaging in circular financing: They are making billions of dollars of long-term purchase commitments, equity investments, and project co-development agreements with one another. OpenAI, Oracle, CoreWeave, and Nvidia are at the center of this web. Nvidia has invested $100 billion in OpenAI, to be repaid over time through OpenAI’s lease of Nvidia GPUs. Oracle is spending $40 billion on Nvidia GPUs to power a data center it has leased for 15 years to support OpenAI, for which OpenAI is paying Oracle $300 billion over the next five years. OpenAI is paying CoreWeave over the next five years to rent its Nvidia GPUs; the contract is valued at $11.9 billion, and OpenAI has committed to spending at least $4 billion through April 2029. OpenAI already has a $350 million equity stake in CoreWeave. Nvidia has committed to buying CoreWeave’s unsold cloud computing capacity by 2032 for $6.3 billion, after it already took a 7% stake in CoreWeave when the latter went public. If you’re feeling dizzy, count yourself lucky: These deals represent only a fraction of the available examples of circular financing.

These companies are all betting on each others’ growth; their growth projections and purchase commitments are all dependent on their peers’ growth projections and purchase commitments. Optimistically, this roundabouting represents a kind of “risk mutualism,” which, at least for now, ends up supporting greater capital expenditures. Pessimistically, roundabouting is a way for these companies to pay each other for goods and services in any way except cash — shares, warrants, purchase commitments, token reservations, backstop commitments, and accounts receivable, but not U.S. dollars. The second any one of these companies decides it wants cash rather than a commitment is when the music stops. Chances are, that company needs cash to pay a commitment of its own, likely involving a lender.

Lenders are the final piece of the puzzle. Contrary to the notion that cash-rich hyperscalers can finance their own data center buildout, there has been a record volume of debt issuance this year from companies such as Oracle and CoreWeave, as well as private credit giants like Blue Owl and Apollo, which are lending into the boom. The debt may not go directly onto hyperscalers’ balance sheets, but their purchase commitments are the collateral against which data center developers, neocloud companies like CoreWeave, and private credit firms raise capital. While debt is not inherently something to shy away from ― it’s how infrastructure gets built ― it’s worth raising eyebrows at the role private credit firms are playing at the center of this revenue-free investment boom. They are exposed to GPU financing and to data center financing, although not the GPU producers themselves. They have capped upside and unlimited downside. If they stop lending, the rest of the sector’s risks look a lot more risky.

Courtesy of Advait Arun

Courtesy of Advait Arun

A market correction starts when any one of the AI companies can’t scrounge up the cash to meet its liabilities and can no longer keep borrowing money to delay paying for its leases and its debts. A sudden stop in lending to any of these companies would be a big deal ― it would force AI companies to sell their assets, particularly GPUs, into a potentially adverse market in order to meet refinancing deadlines. A fire sale of GPUs hurts not just the long-term earnings potential of the AI companies themselves, but also producers such as Nvidia and AMD, since even they would be selling their GPUs into a soft market.

For the tech industry, the likely outcome of a market correction is consolidation. Any widespread defaults among AI-related businesses and special purpose vehicles will leave capital assets like GPUs and energy technologies like supercapacitors stranded, losing their market value in the absence of demand ― the perfect targets for a rollup. Indeed, it stands to reason that the tech giants’ dominance over the cloud and web services sectors, not to mention advertising, will allow them to continue leading the market. They can regain monopolistic control over the remaining consumer demand in the AI services sector; their access to more certain cash flows eases their leverage constraints over the longer term as the economy recovers.

A market correction, then, is hardly the end of the tech industry ― but it still leaves a lot of data center investments stranded. What does that mean for the energy buildout that data centers are directly and indirectly financing?

A market correction would likely compel vertically integrated utilities to cancel plans to develop new combined-cycle gas turbines and expensive clean firm resources such as nuclear energy. Developers on wholesale markets have it worse: It’s not clear how new and expensive firm resources compete if demand shrinks. Grid managers would have to call up more expensive units less frequently. Doing so would constrain the revenue-generating potential of those generators relative to the resources that can meet marginal load more cheaply — namely solar, storage, peaker gas, and demand-response systems. Combined-cycle gas turbines co-located with data centers might be stranded; at the very least, they wouldn’t be used very often. (Peaker gas plants, used to manage load fluctuation, might still get built over the medium term.) And the flight to quality and flexibility would consign coal power back to its own ash heaps. Ultimately, a market correction does not change the broader trend toward electrification.

A market correction that stabilizes the data center investment trajectory would make it easier for utilities to conduct integrated resource planning. But it would not necessarily simplify grid planners’ ability to plan their interconnection queues — phantom projects dropping out of the queue requires grid planners to redo all their studies. Regardless of the health of the investment boom, we still need to reform our grid interconnection processes.

The biggest risk is that ratepayers will be on the hook for assets that sit underutilized in the absence of tech companies’ large load requirements, especially those served by utilities that might be building power in advance of committed contracts with large load customers like data center developers. The energy assets they build might remain useful for grid stability and could still participate in capacity markets. But generation assets built close to data center sites to serve those sites cheaply might not be able to provision the broader energy grid cost-efficiently due to higher grid transport costs incurred when serving more distant sources of load.

These energy projects need not be albatrosses.

Many of these data centers being planned are in the process of securing permits and grid interconnection rights. Those interconnection rights are scarce and valuable; if a data center gets stranded, policymakers should consider purchasing those rights and incentivizing new businesses or manufacturing industries to build on that land and take advantage of those rights. Doing so would provide offtake for nearby energy assets and avoid displacing their costs onto other ratepayers. That being said, new users of that land may not be able to pay anywhere near as much as hyperscalers could for interconnection or for power. Policymakers seeking to capture value from stranded interconnection points must ensure that new projects pencil out at a lower price point.

Policymakers should also consider backstopping the development of critical and innovative energy projects and the firms contracted to build them. I mean this in the most expansive way possible: Policymakers should not just backstop the completion of the solar and storage assets built to serve new load, but also provide exigent purchase guarantees to the firms that are prototyping the flow batteries, supercapacitors, cooling systems, and uninterruptible power systems that data center developers are increasingly interested in. Without these interventions, a market correction would otherwise destroy the value of many of those projects and the earnings potential of their developers, to say nothing of arresting progress on incredibly promising and commercializable technologies.

Policymakers can capture long-term value for the taxpayer by making investments in these distressed projects and developers. This is already what the New York Power Authority has done by taking ownership and backstopping the development of over 7 gigawatts of energy projects ― most of which were at risk of being abandoned by a private sponsor.

The market might not immediately welcome risky bets like these. It is unclear, for instance, what industries could use the interconnection or energy provided to a stranded gigawatt-scale data center. Some of the more promising options ― take aluminum or green steel ― do not have a viable domestic market. Policy uncertainty, tariffs, and tax credit changes in the One Big Beautiful Bill Act have all suppressed the growth of clean manufacturing and metals refining industries like these. The rest of the economy is also deteriorating. The fact that the data center boom is threatened by, at its core, a lack of consumer demand and the resulting unstable investment pathways is itself an ironic miniature of the U.S. economy as a whole.

As analysts at Employ America put it, “The losses in a [tech sector] bust will simply be too large and swift to be neatly offset by an imminent and symmetric boom elsewhere. Even as housing and consumer durables ultimately did well following the bust of the 90s tech boom, there was a one- to two-year lag, as it took time for long-term rates to fall and investors to shift their focus.” This is the issue with having only one growth sector in the economy. And without a more holistic industrial policy, we cannot spur any others.

Questions like these ― questions about what comes next ― suggest that the messy details of data center project finance should not be the sole purview of investors. After all, our exposure to the sector only grows more concentrated by the day. More precisely mapping out how capital flows through the sector should help financial policymakers and industrial policy thinkers understand the risks of a market correction. Political leaders should be prepared to tackle the downside distributional challenges raised by the instability of this data center boom ― challenges to consumer wealth, public budgets, and our energy system.

This sparkling sector is no replacement for industrial policy and macroeconomic investment conditions that create broad-based sources of demand growth and prosperity. But in their absence, policymakers can still treat the challenge of a market correction as an opportunity to think ahead about the nation’s industrial future.